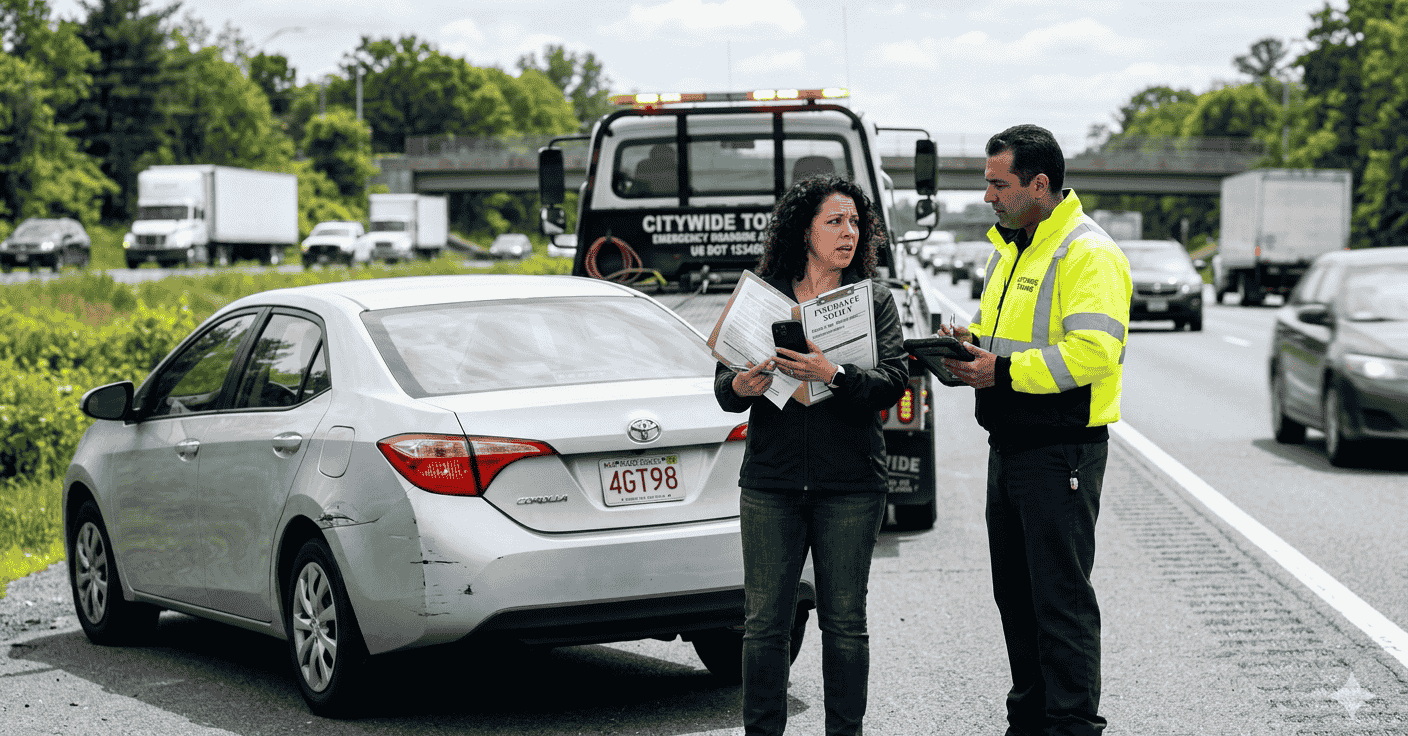

Getting your car towed is stressful enough. But what happens when the tow truck damages your vehicle?

You have rights. Towing companies are responsible for damage they cause during transport.

Here's everything you need to know about towing damage claims. You'll learn how to document damage, file claims properly, and get the compensation you deserve.

What Types of Damage Can You Claim?

Towing companies can damage your car in several ways. Knowing what to look for helps you build a stronger case.

Body and Paint Damage: Scratches, dents, and scrapes happen when operators aren't careful. The tow truck's equipment can scratch your car's surface. Common causes include improper chain placement, dragging against the truck bed, or contact with winch cables. Paint transfer from tow truck equipment is also frequent, especially on darker colored vehicles where marks show more easily.

Wheel and tire damage occurs frequently. Improper wheel-lift positioning can bend rims or damage tires. Sidewall punctures from tow truck arms are particularly common on low-profile tires. Different tow truck types pose different risks to your vehicle.

Transmission Problems: This is serious. Towing a car incorrectly can destroy the transmission. All-wheel-drive vehicles are especially vulnerable. Automatic transmissions can overheat when towed with drive wheels on the ground. Manual transmissions face different risks but can still suffer internal damage from improper towing procedures.

Interior damage includes broken windows, damaged seats, or missing items. Some operators enter vehicles to release parking brakes or shift gears. Dashboard components can crack from rough handling, and personal belongings sometimes disappear during the towing process.

Undercarriage Damage: Low cars can get scraped loading onto flatbeds. Exhaust systems and oil pans are common victims. Plastic underbody panels frequently tear or break during loading. Suspension components can also suffer damage from improper lifting points or excessive ground contact during loading.

Electronic issues sometimes develop after towing. Airbag lights, check engine lights, or electrical problems can result from improper handling. Modern vehicles with sensitive electronic systems are particularly vulnerable to electrical surges or disconnections during towing operations.

How Much Are Towing Damage Claims Worth?

Claim values vary widely based on damage severity and vehicle value. Here's what you can expect.

| Damage TypeTypical Cost RangeSettlement Success Rate | ||

| Minor scratches/paint | $300-$1,500 | 85% |

| Dents and body damage | $500-$3,000 | 80% |

| Wheel/tire damage | $200-$2,000 | 90% |

| Transmission damage | $3,000-$8,000 | 60% |

| Total loss claims | Vehicle value | 40% |

Minor cosmetic damage settles quickly. Major mechanical problems take longer but pay more.

Vehicle age affects settlements. Newer cars get higher payouts than older vehicles. Insurance companies consider depreciation when calculating offers. Luxury vehicles typically receive higher settlements due to expensive parts and specialized repair requirements.

Warning: Don't accept the first offer. Initial settlements are usually low. Most people can negotiate higher amounts with proper documentation.

When Should You Document Damage?

Time is critical for towing damage claims. The sooner you document everything, the stronger your case becomes.

Before the Tow: Take photos of your car from all angles before the tow truck arrives. This proves pre-existing condition. Include close-ups of any existing scratches, dents, or wear patterns. Time-stamped photos provide the strongest evidence.

During pickup, watch the loading process. Note any rough handling or improper equipment use. Don't be afraid to speak up if something looks wrong. Record video if possible, as it captures the sequence of events better than still photos.

Immediately After Delivery: Inspect your vehicle thoroughly before the driver leaves. Look for new damage that wasn't there before.

Check these areas carefully:

- All four corners of the vehicle

- Bumpers and side panels

- Wheels and tires

- Undercarriage (use your phone's flashlight)

- Interior condition

- Hood and trunk alignment

- Door operation and window function

- Exhaust system and visible mechanical components

Take photos immediately. Good lighting helps show damage clearly. Get close-up shots and wide angles for context.

Document everything in writing. Note the date, time, weather conditions, and driver's name. This creates a paper trail.

What Evidence Do You Need to Win?

Strong evidence makes or breaks towing damage claims. Here's what successful claimants collect.

Photo Evidence: Take at least 20 photos showing damage from multiple angles. Include the tow truck, your car, and the scene.

Get the tow truck's license plate and company information. Photos of their equipment help prove what caused the damage.

Written Documentation: Get a copy of the tow receipt. It should include the driver's name, company information, and pickup/delivery details.

Write down exactly what happened while it's fresh in your memory. Include conversations with the driver or any witnesses.

Professional Estimates: Get repair estimates from at least two licensed mechanics. This establishes damage costs and proves the work is necessary.

Ask mechanics to specify which damage is new versus pre-existing. Their expert opinion carries weight with insurance companies.

Keep all receipts for towing fees, rental cars, and other expenses. You can claim these costs too. Understanding typical towing costs helps identify overcharges.

How Do You File a Towing Damage Claim?

Filing claims properly increases your success rate. Follow these steps exactly.

Step 1: Contact the towing company first. Many settle small claims quickly to avoid insurance involvement.

Call within 24 hours of discovering damage. Be polite but firm about your claim. Ask for their insurance information.

Step 2: File with their insurance company. Most towing companies carry commercial liability insurance covering customer vehicle damage.

Submit your claim in writing. Include all photos, estimates, and documentation. Send via certified mail to prove delivery.

Step 3: Follow up regularly. Insurance companies often delay hoping you'll give up. Call weekly for status updates.

Keep detailed records of all communications. Note who you spoke with, when, and what they said.

Step 4: Consider your own insurance. If the towing company won't cooperate, file with your comprehensive coverage.

Your insurance company will investigate and pursue the towing company for reimbursement. This is called subrogation.

What Are Your Rights During Towing?

Knowing your rights helps prevent damage and strengthens claims when problems occur.

You can inspect your vehicle before and after towing. Don't let anyone rush you through this process.

Towing companies must use proper equipment for your vehicle type. Your rights during a tow include refusing service if they lack appropriate equipment.

Right to Refuse: You can reject a tow if the operator seems inexperienced or uses wrong equipment.

You have the right to be present during loading and unloading. Some companies try to rush customers away from the scene.

Documentation Rights: Request copies of all paperwork. This includes tow receipts, damage reports, and insurance information.

State laws vary on towing rights. Towing laws by state explain specific protections in your area.

Note: This is general information, not legal advice. Check your state's specific laws for details.

How Do Insurance Companies Handle Towing Claims?

Understanding how insurers process claims helps you navigate the system better.

Initial Review: Insurance adjusters first determine if damage occurred during towing. They compare before and after photos.

Adjusters investigate by interviewing the driver, reviewing company records, and inspecting your vehicle.

Damage Assessment: Professional appraisers evaluate repair costs. They distinguish between towing damage and pre-existing issues.

Insurance companies often try to blame pre-existing damage. Strong documentation from before the tow counters this argument.

Settlement Negotiations: Initial offers are usually low. Insurers expect negotiation and often increase amounts when pressed.

Don't accept the first offer unless it covers all your costs. Most successful claimants negotiate 20-40% higher settlements.

Major insurers like GEICO, Progressive, and State Farm handle towing damage claims regularly. Their processes are similar but timelines vary.

Prices from providers like AAA, GEICO, and Progressive are current as of 2026. We're not affiliated with these companies.

What Common Mistakes Kill Towing Claims?

Avoiding these mistakes dramatically improves your chances of winning.

Poor Documentation: Blurry photos or missing evidence weakens your case. Take time to document thoroughly. Use your phone's camera settings to ensure high-resolution images that clearly show damage details.

Waiting too long to file claims is deadly. Most policies require notification within 30 days of damage discovery. Some states have even shorter deadlines, so act quickly.

Accepting Verbal Agreements: Get everything in writing. Verbal promises from tow drivers mean nothing legally. Even friendly drivers who promise to "take care of everything" may not follow through once they leave the scene.

Not getting multiple repair estimates hurts negotiations. Single estimates look biased to insurance companies. Three estimates from different shops provide the strongest foundation for your claim.

Admitting Fault: Never admit your car had pre-existing damage unless you have proof. Let evidence speak for itself. Insurance adjusters are trained to look for admissions of fault that can reduce claim values.

Failing to preserve evidence is costly. Don't repair damage before insurance inspection unless it's unsafe to drive. Emergency repairs should be documented and pre-approved when possible.

Not Reading Fine Print: Towing contracts sometimes limit liability. Understanding these terms helps set realistic expectations. However, many liability limitations are unenforceable under state consumer protection laws.

Choosing the wrong tow company increases damage risk. Research reliable towing companies before you need service.

When Should You Hire a Lawyer?

Most towing damage claims settle without legal help. But some situations require professional assistance.

High-Value Claims: Damage over $5,000 warrants legal review. Lawyers can maximize settlements for expensive repairs.

Total loss claims almost always need lawyers. These cases involve complex valuations and liability questions.

Insurance Company Denial: If insurers refuse to pay legitimate claims, lawyers can force cooperation through legal pressure.

Bad faith insurance practices justify legal action. This includes unreasonable delays, lowball offers, or claim denials without investigation.

Personal Injury: If towing damage caused accidents resulting in injuries, lawyers become essential.

Most personal injury lawyers work on contingency. They only get paid if you win, making legal help accessible.

Warning: Lawyer fees can exceed small claim values. Calculate potential recovery before hiring representation.

How Can You Prevent Towing Damage?

Prevention is always better than filing claims. These steps reduce damage risk significantly.

Choose Reputable Companies: Research towing companies before needing service. Find towing services near you with good reviews and proper licensing.

AAA and insurance company partners usually maintain higher standards than random roadside operators.

Vehicle Preparation: Prepare your vehicle properly before the tow truck arrives.

Remove valuable items and secure loose parts. This prevents theft claims and additional damage.

Communication: Tell the driver about special considerations. Low cars, modified suspensions, or all-wheel-drive systems need special handling.

Stay present during loading. Politely point out potential problems before damage occurs.

Equipment Matching: Ensure the tow truck has appropriate equipment. Flatbed trucks are safest for most vehicles.

Wheel-lift trucks work for standard cars but can damage low or modified vehicles.

What State Laws Affect Towing Claims?

State regulations impact towing damage claims in several ways. Here's what varies by location.

| StateClaim Filing DeadlineMinimum Insurance RequiredSpecial Protections | |||

| California | 30 days | $1 million liability | Written damage reports required |

| Texas | 60 days | $500,000 liability | Pre-tow vehicle inspection rights |

| Florida | 45 days | $300,000 liability | Mandatory tow receipts |

| New York | 30 days | $1 million liability | Consumer complaint process |

| Illinois | 90 days | $750,000 liability | Damage disclosure requirements |

Licensing Requirements: Most states require towing companies to carry commercial insurance. Minimum amounts vary from $100,000 to $1 million.

Some states mandate specific training for tow truck operators. This reduces damage rates in states with strict requirements.

Consumer Protections: States like California require written damage reports before and after towing. This creates automatic evidence for claims.

Other states allow verbal agreements, making documentation more important for consumers.

Check your state's Department of Transportation website for specific towing regulations and consumer rights.

How Long Do Towing Damage Claims Take?

Claim timelines vary based on damage severity and insurance company cooperation.

Simple Claims (Under $1,000): These usually settle within 2-4 weeks. Clear documentation speeds the process.

Insurance companies prioritize small claims to avoid administrative costs.

Moderate Claims ($1,000-$5,000): Expect 4-8 weeks for settlement. These require more investigation and multiple estimates.

Adjusters may inspect your vehicle personally for mid-range claims.

Complex Claims (Over $5,000): Major damage claims can take 3-6 months. Total loss claims take the longest.

These cases often involve multiple experts, extensive documentation review, and legal considerations.

Disputed Claims: When liability is contested, claims can drag on for months or years. Strong initial documentation prevents most disputes.

Consider your own insurance coverage for faster resolution of disputed claims.

Your insurance company can pursue the towing company while you get repairs started immediately.

What Happens After You Win Your Claim?

Winning your towing damage claim is just the first step. Here's what comes next.

Payment Processing: Insurance companies typically issue checks within 5-10 business days of settlement agreement.

Large claims may require additional verification before payment release.

Repair Authorization: Some insurers want to approve repair shops before you start work. Others let you choose any licensed facility.

Get written authorization before beginning expensive repairs to avoid payment disputes.

Supplemental Claims: Additional damage sometimes appears during repairs. Most policies cover these discoveries if reported promptly.

Take photos of hidden damage and notify the insurance company immediately.

Rental Car Coverage: Many policies include rental car reimbursement during repairs. Keep all receipts for submission.

Economy cars are usually covered. Upgrades come out of your pocket unless specifically authorized.

Final Documentation: Keep all claim documents for tax purposes. Damage settlements may be taxable depending on circumstances.

Consult a tax professional for advice on reporting insurance settlements.

Remember that winning a claim doesn't prevent future damage. Get a free towing quote from reputable companies to avoid problems next time.

Quality towing companies invest in proper equipment and training to minimize damage risks. The extra cost is worth avoiding claim hassles.

Pro Tips for Maximizing Your Settlement

Experienced claim handlers use these strategies to increase settlement amounts and speed up the process.

Document Everything Twice: Keep digital copies of all photos and documents in cloud storage. Physical documents can be lost, but digital backups ensure you never lose critical evidence.

Create a detailed timeline of events. Insurance adjusters appreciate organized presentations that clearly show the sequence of damage occurrence.

Use Professional Language: When communicating with insurance companies, use formal business language. Avoid emotional appeals and stick to facts. This positions you as a serious claimant who understands the process.

Reference specific policy language when making your case. Insurance companies respond better to claimants who understand coverage terms and exclusions.

Leverage Market Rates: Research typical repair costs in your area before accepting settlements. Insurance companies sometimes offer below-market rates, hoping claimants won't verify pricing.

Get estimates from both dealership service centers and independent shops. This gives you a range to negotiate within and shows you've done your homework.

Know When to Escalate: If initial adjusters aren't responsive, ask to speak with supervisors. Most insurance companies have escalation procedures for difficult claims.

State insurance commissioners can intervene in disputes. Filing complaints with regulators often motivates insurance companies to resolve claims quickly.

Frequently Asked Questions

Need Emergency Towing Services?

Don't wait when you're stranded. Get professional help now.

Find Trusted Towing Services

Discussion (0)

Be the first to comment!

Share your experience or ask questions about towing services.