What's the Real Difference Between Repo and Emergency Towing?

Here's the thing: repo towing and emergency towing are completely different services. They operate under different laws, cost different amounts, and serve opposite purposes.

Repo towing happens when a lender hires a company to recover a vehicle. You missed payments, and the lender wants their asset back. It's involuntary. You don't call them—they come for your car.

Emergency towing is what you call when your car breaks down on the highway. Your engine dies. You get in an accident. You need help right now. This is voluntary and customer-initiated.

Understanding these differences matters. It affects your legal rights, your costs, and what you should do if either situation happens to you.

Why Do Repo Companies Tow Vehicles?

Repo towing exists because lenders need a way to recover vehicles when loans go bad. You signed a contract. You agreed to make monthly payments. When you stop paying, the lender loses money.

The loan agreement actually gives the lender the right to repossess. It's written into your paperwork. Most people don't read it carefully, but it's there.

Here's what triggers a repo:

- Missing one payment in most states (some require two or three)

- Being significantly behind on your loan

- Violating other loan terms (like driving without insurance)

- Filing for bankruptcy

The lender doesn't need a court order to repossess. They just need reasonable cause to believe you've defaulted. This is called "self-help repossession" in legal terms.

Once they take your car, it goes to an auction. Money from the sale pays off the loan. If the sale doesn't cover the full debt, you might owe the difference (called a "deficiency").

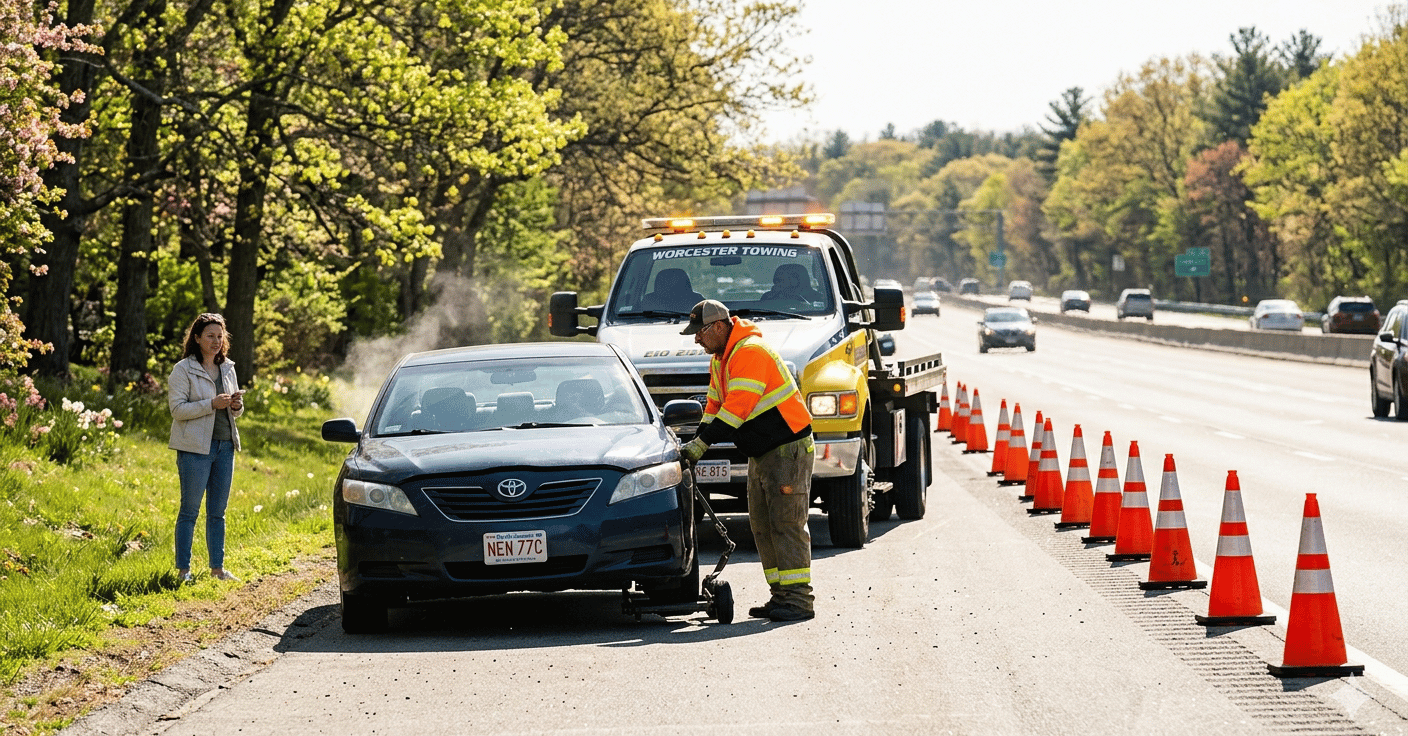

Why Do People Call Emergency Towing Services?

Emergency towing helps when your vehicle can't move on its own. You're the one requesting help because you need it.

Common reasons people call emergency tow trucks:

- Engine failure or mechanical breakdown

- Flat tires that can't be changed

- Dead battery that won't jump-start

- Out of fuel and no gas station nearby

- Accident damage that prevents driving

- Transmission problems

- Stuck in snow, mud, or off the road

- Lockouts where your keys are inside the car

You call a tow truck company, roadside assistance provider, or your auto insurance company. They dispatch a truck to your location. You pay for the service, and your vehicle goes where you want it (usually a repair shop).

This is a straightforward transaction. You need help. You pay for it. Done.

How Does the Legal Authority Differ?

The legal foundation for repo towing and emergency towing couldn't be more different.

Repo Towing Legal Authority:

Repo companies operate under the Uniform Commercial Code (UCC) and state-specific repossession laws. Your loan agreement grants them this authority. However, there are limits.

Warning: Repo companies cannot use force or breach the peace. They can't damage your property, threaten you, or break into your garage. They can't tow your car if you're in it. If they violate these rules, you can sue them.

Some states require lenders to notify you before repossessing. Others don't. Check your state's laws—this matters for your rights. Learn more about towing laws by state and your rights.

Emergency Towing Legal Authority:

Emergency towing requires your consent (or your insurance company's consent if you have roadside assistance). The tow company is providing a service you requested. They don't need special legal authority beyond a business license.

You decide where the car goes. You control the transaction. You have full consumer protection rights.

State consumer protection laws apply to emergency towing. If a company overcharges or damages your vehicle, you can file a complaint or lawsuit. Learn more about your rights during a tow.

What Are the Cost Differences?

Pricing for repo towing and emergency towing varies widely. But they're structured differently.

| Service Type | Typical Cost Range | Who Pays | Distance Factor |

|---|---|---|---|

| Repo Towing | $150–$400 per tow | Lender (added to debt) | Usually short distance |

| Emergency Towing | $75–$300 per tow | Vehicle owner or insurance | Varies widely |

| Long-Distance Towing | $1–$4 per mile | Vehicle owner or insurance | Charged for each mile |

| Storage Fees | $25–$75 per day (repo) | Added to your debt | Compounds quickly |

Repo towing costs: The lender pays the repo company. But you end up paying because these costs get added to your loan debt. If your car sells for $8,000 and the tow cost $300, you owe the difference between $8,300 and what the car actually sells for.

Storage fees are brutal. If your car sits in a repo lot for 10 days at $50 per day, that's $500 added to your debt. Many people don't realize this.

Emergency towing costs: You pay directly, or your insurance covers it. Basic towing usually runs $100–$200 for a local tow. Long-distance towing is priced per mile.

If you have roadside assistance through AAA, GEICO, Progressive, or State Farm, your costs might be covered entirely. Check your policy. Prices from providers like these are current as of 2026. We're not affiliated with these companies.

For more details on pricing, read how much towing costs in 2025.

Who Can Legally Perform Each Type of Tow?

Not every tow truck company can do repo work. Not every repo company wants to do emergency towing. These are different skill sets and business models.

Repo Towing Companies:

Repo companies specialize in vehicle recovery. They're licensed and bonded. They work directly with lenders, finance companies, and auto dealers. Many operate 24/7 because repossessions happen anytime.

Repo operators train specifically for this work. They learn how to locate vehicles, bypass security systems (legally), and handle confrontational situations. They understand the laws that govern repossession in each state.

Repo companies often use GPS tracking and databases to find vehicles. They coordinate with lenders and maintain detailed records for legal protection.

Emergency Towing Companies:

Emergency tow truck operators need a business license and insurance. They don't need special repossession training or licensing. Most towing companies offer emergency services.

They might operate locally or regionally. Some are independent; others work for large chains. AAA members use emergency towing frequently—AAA contracts with local providers in each area.

Emergency towing operators focus on customer service. They need to communicate clearly, arrive quickly, and handle stressed drivers professionally.

Many emergency towing companies also offer repo services as a side business. But they're not specialists in repossession.

What Happens After the Tow?

This is where repo and emergency towing diverge completely.

After Repo Towing:

Your car goes to a repo lot or holding facility. The lender now controls your vehicle. You have a window to reclaim it—usually 10 days in most states. During this time, you can pay the full loan balance plus towing and storage fees to get your car back.

If you don't reclaim it, the lender sells it at auction. The auction happens quickly—sometimes within 30 days. You get notice of the sale (in most states), but you can't stop it.

After the sale, you're responsible for any deficiency. If your car sells for $6,000 and you owed $9,000 on the loan, you now owe $3,000. Plus towing and storage fees. The lender can sue you for this amount.

This hurts your credit score. Repossession stays on your credit report for 7 years. It's one of the worst marks possible.

After Emergency Towing:

Your car goes to the location you specified. Usually it's a repair shop. You own it. The tow company has no claim on it.

You pay the tow bill. That's it. No long-term consequences. Your credit isn't affected. There's no debt added to a loan.

You arrange repairs with the shop. You pay for those separately. Everything stays under your control.

Can You Stop a Repo Tow Before It Happens?

Yes. But you need to act fast and know your options.

If you see a repo truck coming for your car:

- Contact your lender immediately. Call the finance company or bank. Explain your situation. Ask about loan modification, deferment, or payment plans.

- Offer to catch up payments. Many lenders will pause the repo if you pay the missed amount plus late fees.

- Ask about refinancing. Some lenders will work with you if you can refinance the loan elsewhere.

- Request a forbearance agreement. The lender might agree to skip one or two payments if you're facing temporary hardship.

- Consult a credit counselor. Nonprofit credit counseling agencies (often free) can negotiate with lenders on your behalf.

The key is reaching out before the repo actually happens. Once the truck has your car, it's much harder to recover it.

Warning: Don't ignore collection notices or calls. The lender is building a legal case. The sooner you communicate, the better your options.

What Should You Do If You're Stranded and Need Emergency Help?

Emergency towing situations require quick thinking. Here's what to do.

Step 1: Get to Safety

If you're on a highway, turn on hazard lights. Get out of traffic if possible. Move to the shoulder or a safe location. Don't stay in the car if traffic is heavy.

Step 2: Call for Help

Call 911 if there's an accident or you're in immediate danger. Otherwise, call your roadside assistance provider (AAA, insurance company) or a local tow truck company. If you don't have a preferred provider, search "towing near me" or find towing services near you using USA Tow Finder.

Step 3: Provide Clear Information

Give the dispatcher your exact location, vehicle description, and the problem. "My car won't start on Highway 405 near Exit 12" is better than "I'm stuck somewhere."

Step 4: Wait Safely

Lock your doors. Stay alert. If you feel unsafe, wait inside a nearby business or call police for assistance.

Step 5: Check the Quote

When the truck arrives, ask for the price before they hook up your car. Confirm where it's going. Get a receipt. Don't pay in cash if possible—use a card for protection.

For a complete guide, read what to do when your car breaks down.

How Does Insurance Coverage Work for Each Type?

Insurance handles repo and emergency towing very differently.

Emergency Towing and Insurance:

Most comprehensive auto insurance policies include roadside assistance. This covers towing up to a certain distance (usually 5–7 miles). You typically pay a small deductible ($0–$100) or nothing at all.

If you have AAA membership, you get towing coverage separate from insurance. AAA includes up to 100 miles of free towing depending on your membership level.

Roadside assistance through your insurance is the cheapest way to handle emergency towing. Check your policy to see what's included.

Repo Towing and Insurance:

Your auto insurance does not cover repossession. The lender pays for it. Your car loan agreement requires you to maintain insurance, but insurance doesn't protect you from repo.

Some loan agreements require "gap insurance." This covers the difference between what you owe and what the car sells for after repossession. Gap insurance is optional but worth considering if you're financing a vehicle.

For details on what's covered, read the towing insurance coverage guide.

What Are Your Consumer Rights in Each Situation?

Your legal protections differ dramatically depending on which type of tow you're dealing with.

Rights During Emergency Towing:

You have strong consumer protections. The tow company must provide honest pricing. They can't damage your vehicle intentionally. They must deliver your car safely to the location you specified.

If they overcharge you, you can dispute the charge with your credit card company or insurance. You can file a complaint with your state's attorney general. You can sue for damages.

You have the right to know the company's pricing before the tow. You have the right to choose where your car goes (unless insurance is paying and has restrictions).

Rights During Repossession:

Your rights are more limited, but they still exist. The repo company cannot breach the peace. They can't use violence or threats. They can't damage your property beyond what's necessary for the tow.

They cannot tow your car if you're sitting in it. They cannot enter your garage or home without permission. If they do, they've violated your rights and you can sue.

You have the right to redeem your vehicle (pay the full loan balance plus fees) within the redemption period—usually 10 days.

You have the right to notice before the car is sold. In most states, the lender must send written notice of the sale. You can attend the auction and bid on your own car if you want.

You have the right to sue for damages if the repo company violates the law. Many people win these cases.

Learn more about your rights during a tow.

How Common Are Repo Tows vs Emergency Tows?

Industry data shows emergency towing is far more common than repossession.

Emergency Towing Statistics:

Americans call for emergency roadside assistance approximately 33 million times per year. That's roughly 1 in 10 vehicles needing help. AAA alone responds to about 30 million calls annually.

The most common reasons for emergency tows are dead batteries, flat tires, lockouts, and mechanical failures. Winter months see a spike in towing calls due to weather-related breakdowns.

Repossession Statistics:

Approximately 2 million vehicles are repossessed annually in the United States. That's about 0.6% of all vehicles on the road. Repossessions have increased as inflation pushes more people behind on car payments.

The average person who experiences repossession is behind on payments by 3–4 months. Most repossessions happen on financed vehicles, not leased ones.

For more industry insights, read towing industry statistics for 2026.

Which Type of Tow Should You Prepare For?

Realistically, you're much more likely to need emergency towing than to experience repossession. But preparation matters for both.

To Avoid Repossession:

- Make your car payments on time, every time

- If you're struggling, contact your lender immediately

- Explore loan modification or forbearance options early

- Don't ignore collection notices

- Consider gap insurance when financing a vehicle

To Handle Emergency Towing:

- Get roadside assistance through AAA or your insurance

- Keep a list of local tow truck numbers in your phone

- Maintain your vehicle regularly to prevent breakdowns

- Keep your insurance and registration in the car

- Know your vehicle's towing capacity if you tow trailers

For vehicle maintenance, read how to prepare your vehicle for towing.

Key Takeaways: Repo vs Emergency Towing

Repo towing and emergency towing are fundamentally different services operating under different rules.

Repo towing: Involuntary recovery of vehicles for lenders. Triggered by missed payments. Adds costs to your debt. Damages credit for 7 years. Limited consumer protections but legal restrictions on the repo company.

Emergency towing: Voluntary roadside assistance for breakdowns and accidents. You request the service. You pay directly. No credit impact. Strong consumer protections. Covered by insurance in most cases.

The best strategy is preventing repossession through responsible payments and addressing financial problems early. For emergency towing, maintain your vehicle and keep roadside assistance active.

If you need towing services right now, find trusted towing providers on USA Tow Finder. We help you locate reliable, licensed, and insured tow truck companies in your area.

Understanding these differences protects your wallet and your rights. Don't wait until you're in crisis to learn how towing works.

Frequently Asked Questions

Need Emergency Towing Services?

Don't wait when you're stranded. Get professional help now.

Find Towing Services Near You

Discussion (0)

Be the first to comment!

Share your experience or ask questions about towing services.